The Fed, The President, and The Stablecoins

August Commentary

As US President Trump becomes increasing vocal in his desire to replace the Fed Chair Jerome Powell and data released in August proved the US economy to be on a weaker footing, expectations rose for a rate cut in September. Indeed, on September 17, the Fed delivered with a 25 bps rate cut, dropping the target range to 4%-4.25%. But if lower rates stimulate a risk asset like BTC, how do we explain BTC posting a -6.49% drop in August? Is it because August tends to be a weak month for risk assets, equities and crypto alike? Over the last 13 years, as compiled by Coinglass, Bitcoin has returned an average return of +1.12% in August, a median of -7.49%, and returned negatively in 9 of the past 13 instances. Or are the markets afraid of the Fed losing its independence leading to rising inflation and rising long-term rates, upon which risk assets are priced?

Risks From Loss of Central Bank Independence

The economic risk of ceding monetary policy to a President’s control isn’t just academic. One only needs to look at Turkey whose President Recep Tayyip Erdogan decided to pursue a low interest rate policy in late 2021 to boost the economy, despite the presence of inflationary pressures.

Source: Trading Economics

The results were catastrophic with the country’s inflation reaching over 80% annualized in late 2022 while short rates stayed below 9%. Only upon winning a third term in mid-2023 did President Erdogan reverse course by hiring a new team of central bankers and giving them leeway to fight inflation.

It is no wonder that as President Trump continues to threaten the Fed independence, bankers are calling out the potential risks to the US economy [1], [2], [3]. However, as many market observers have pointed out, the market, oddly, doesn’t seem to really care.

Source: Trading Economics

Markets are forward-looking and ought to be pricing in the higher risks to US economic stability by weakening the US Dollar and pushing up the long-term yields on US Treasuries. However, after the initial drop to a level of about 100 due to the US tariff threats, the US Dollar Index seems to be trading in a narrow 5% band since the end of April.

Source: Trading Economics

Similarly, the 20- and 30-year yields on US Treasuries have traded under 5% in a narrow range of approximately 50 bps. The recent drops towards the 4.6% level are indicative of the weaker than expected reports that have been released over the past week. While the CPI release came out a tad high at an expected 2.9% annualized rate for August, a revision of -911,000 to the jobs recorded back in March 2025 came as a surprise.

Source: Trading View

Equally surprising, the MOVE Index, which tracks the volatility in the US Treasuries market, is portraying calm, reaching levels last seen before the Fed’s 2022 rate hikes. Do the markets know something that the bankers don’t? Are they very confident that the US Fed will not lose its independence?

Enter the Stablecoins and US Treasury RWAs

The market capitalization of USD stablecoins has been rising from $120 billion in October 2023 to currently around $280 billion, an annualized growth rate of 55%. USD-pegged stablecoins dominate this market, with a market share of 99%. With the GENIUS Act becoming law on July 18, 2025, reserve-backed stablecoins are emerging as the dominant form of stablecoins, and US Treasuries are emerging as the favoured collateral.

USDT (Tether) and USDC dominate the stablecoin arena with their respective $169 billion and $72 billion in capitalization. The rise of USD stablecoins since 2021 has created a new source of demand for US Treasury bills. USDT holds around 80% of its assets in US treasury bills according to Tether’s audit report. As disclosed in its latest financials, Circle backs its USDC with its Circle Reserve Fund which is being managed by Blackrock and holds roughly 45% in Treasury bills and 55% in repurchase agreements backed by US Treasury collateral.

However, new entrants are forming. USDtb is a stablecoin that has been trading for around 9 months, is in part backed by Blackrock’s BUIDL token, and has a $1.8 billion capitalization. The Trump family’s World Liberty Financial issued their USD1 token in April 2025, backed by USD and government money market funds, and has about $2.7 billion in market cap. Just announced on September 14, Hyperliquid, a wildly popular Layer 1 DEX, voted to have Native Markets issue a new stablecoin USDH on their chain that is “fully backed by cash and US treasury equivalents”.

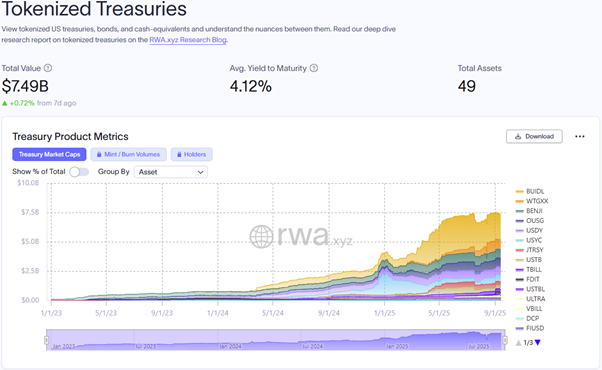

Meanwhile, tokenized US Treasuries make up a small but quickly growing portion of the tokenized real-world assets (RWAs).

Source: rwa.xyz

Over the last year, these assets have grown from approximately $2.1 billion to currently $7.5 billion, a 3.6-fold increase. Unlike stablecoins, the valuations of these tokens fluctuate with prices of the underlying securities but they offer real world USD yields, something that crypto investors covet.

The Marginal Buyer

The total US Federal debt currently stands at $36 trillion, of which $6.4 trillion is financed by short-dated Treasury bills and the remainder by notes, bonds, and non-marketable securities. Furthermore, the US Congressional Budget Office estimated that the recently passed One Big Beautiful Act will add another $3 trillion to the debt over the next 10 years.

The Federal Reserve Bank of Kansas City had released a study (Part 1, Part 2) that showed that foreign holdings of US Treasuries have steadily declined from its peak of 60% in 2010 to now below 40%. Aside from the Federal Reserve purchases, foreign buyers have been replaced domestically by money market funds, hedge funds, and households. Continuing to find willing buyers for a growing stockpile of US debt is a concern at the top of the mind for many bankers and the current administration.

Today, stablecoins and tokenized US Treasuries currently total $288 billion, making up less than 5% of the outstanding US Treasury bills, the type of securities that this group is currently focused on buying. The growth of stablecoins alone, however, is forecasted to be stratospheric. While JP Morgan estimated that the stablecoin market may grow to $500 billion by 2028, Standard Chartered has placed that estimate at $2 trillion over the same time period. It’s further conceivable that tokenized longer-dated Treasuries may find its own product market fit in DeFi portfolios, trading, and collateral usage for derivatives.

Are these the expectations that have been keeping long-term US rates stable and overruling any concerns that the market may have about the loss of Fed independence? It is still too early to tell, and naysayers abound on the benefits of the role that stablecoins may play. The Kansas City Fed thinks that while stablecoins may increase their demand for Treasuries, it may simply be supplanting other traditional buyers as well as adversely reducing the banks’ ability to create credit. What is clear is that stablecoins are not the boring USD pegged on-chain payment facilitator that lurks in the background. Together with tokenized Treasuries, this group of tokens has the potential to influence how interest rates are determined, the very elements that determine how much interest the US Treasury needs to pay, how risk assets are priced, and how economies unfold.