Walled Gardens 2.0

Through September and early October, macroeconomic news has captured investor attention. While BTC posted a +5% gain in September, market volatility has increased in light of the US government shutdown now expected by Polymarket to last over 30 days, creeping unemployment without having any official data to verify, and gold prices reaching over $4,000 indicating a higher level of market stress. Investor attention was further drawn to US President Trump’s announcement of new tariffs on China and the subsequent crypto-market deleveraging that ensued. One can be forgiven for not noticing that through the summer of 2025, Silicon Valley quietly redrew the map of finance.

Starting in August, within weeks of each other, Circle, Stripe, and Google each unveiled their own Layer-1 (L1) blockchains. Circle debuted Arc on August 12th with its quarterly earnings report. A month later, Stripe followed with Tempo, a “payments-first” blockchain built with Paradigm, a crypto asset fund manager. Google Cloud, never one to be left behind, pushed ahead with its Google Cloud Universal Ledger (GCUL) after trial runs with the CME Group. The world’s largest fintech and tech firms are opting to build their own blockchains instead of relying on public blockchains.

The Case for the Corporate Chain

Supporters say this shift is overdue. As Stripe’s Patrick Collison put it, public blockchains “are not optimized for growing stablecoin traction.” Public blockchains, for all their innovation, haven’t quite yet met the demands of traditional finance. Gas fees spike unpredictably. Regulatory compliance remains challenging. And security, while robust, often comes at the expense of usability. Understandably, financial institutions prefer predictability, control, and the TradFi user experience.

Corporate Layer-1s promise exactly that:

Predictable economics, with low and stable fiat-denominated fees, payable in stablecoins rather than volatile crypto tokens.

Regulatory comfort, through KYC-verified accounts and compliance-friendly privacy tools.

Speed and scalability, capable of handling institutional transaction volumes in real time.

What’s not to like? Private blockchains would offer banks, custodians, exchanges, and regulators a shared ledger which would save time and money from each entity owning their own ledgers and reconciling among themselves. Arguably, why not ask Google or Oracle to just create and maintain one giant financial ledger, structured as a traditional SQL database for these entities?

”Holy Cow, I need a piece of the pie”

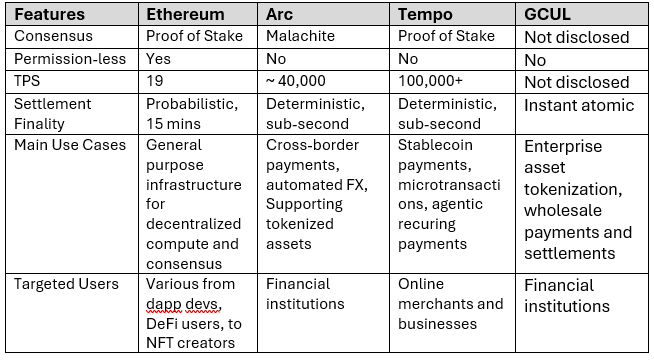

Each of these new blockchains is engineered for scale and settlement finality. Tempo aims to process over 100,000 transactions per second with sub-second finality, using stablecoins as gas fees to make costs both predictable and fiat-denominated. Arc is EVM-compatible and runs on its own Malachite consensus engine, achieving finality in 350 milliseconds while offering optional privacy via “view keys” for regulators. GCUL is positioned as "credibly neutral" infrastructure open to any financial institution. However, only KYC-verified entities can transact, and contracts are written in Python, an open-source language familiar to banks and machine-learning engineers alike.

Sources: Firinne Capital, documentation from Circle, Stripe, Paradigm, Circle and Google, chainspect.app, cryptosettlementtime.com

Indeed, transaction speeds are expected to improve by orders of magnitudes when compared to the largest smart-contract enabled L1, Ethereum. The blockchain trilemma posits that blockchain designs need to trade-off against the three characteristics of scalability, security, and decentralization and for better or worse, it seems that these newly formed L1s seek to improve scalability by forsaking decentralization. Diving into Arc’s litepaper reveals that its Malachite consensus “allows for deterministic finality with a permissioned set of established validators to guarantee the integrity of the network.” Furthermore, “Arc will rely on a permissioned, Proof-of-Authority (PoA) validator set composed of a limited number of known, established, and geographically distributed institutions held to high standards of accountability and operational guarantees.”

If one of the original promises of blockchain from 2009 was about decentralization, this new phase seems to be about recentralization for the promise of scalability while enacting enterprise controls. Stablecoins already enable its issuer to capture the net interest margin for itself while promising its token will maintain its peg to a fiat currency. By also controlling their own Layer-1s, these companies can further dictate how fees are priced, how data is shared, and how regulations are to be interpreted and complied with. They are not merely using blockchain technology; they are rewiring them to suit their enterprise priorities.

”Tear down this wall!”

- Ronald Reagan, June 1987

To critics, this moment feels like déjà vu. Web 3’s promise of decentralization and privacy was in response to Web 2’s surveillance capitalism, characterized by walled gardens carved by corporate platforms [1]. Now, the same erosion may be unfolding in blockchain-based finance. It’s hard to conceive that a blockchain run by a single firm can be “credibly neutral.” Its rules can be rewritten, its users censored, and its liquidity trapped in silos. Instead of one global ledger for value, the world could splinter into dozens of fast but incompatible corporate networks, each compliant, performant, and fundamentally closed.

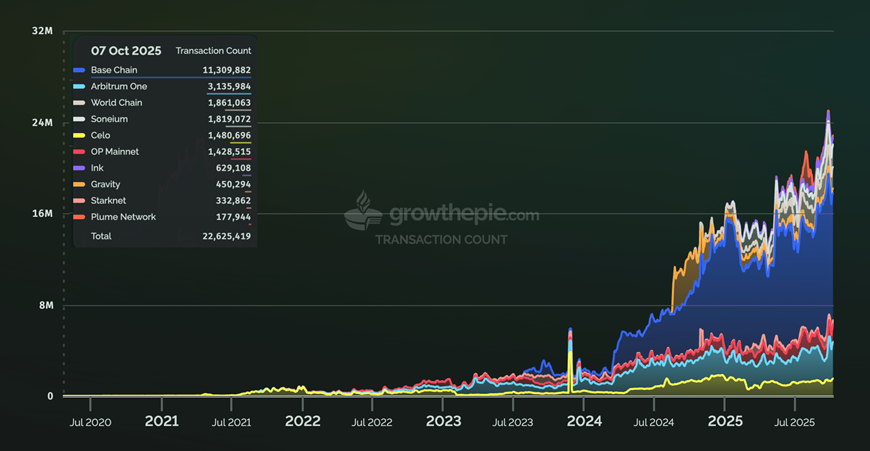

Ethereum supporters see this trend as a departure from crypto’s founding ideals of decentralization and composability. They argue that corporate Layer-1s bypass Ethereum’s mature Layer-2 (L2) ecosystem, which include Arbitrum and Coinbase’s Base, that already provide scalability, security, and liquidity.

Stacked Daily Transactions on Top 10 Ethereum L2 networks

Source: Growthepie.com

By building independent chains, companies such as Circle, Stripe, and Google are choosing proprietary control over interoperability, fragmenting the ecosystem and weakening Ethereum’s position as the internet’s open financial backbone.

The New Neutrality Test

Ethereum now faces a challenge that is more political than technical. History suggests open standards tend to outlast proprietary ones. For example, the open TCP/IP protocol became the global standard for computer networking. The global adoption of the standard gauge (1,435 mm) replaced regional and company-specific proprietary rail gauges. Can the chain adapt and be adopted fast enough to bridge the gap between the trustless and trusted, between the freedom of code and the comfort of compliance such that it remains the neutral settlement layer that underpins both open and corporate networks?

Centralization and decentralization are like yin and yang. Decentralization promotes creativity but makes coordination difficult and costly. Centralization promises efficiency but stifles creativity, neutrality, and interoperability. The world needs both to be balanced. How much centralization does the world need? Likely not 100% but perhaps it’s better to leave it to the market and its participants to decide.