America's Crypto Manifest

July 2025 Commentary

It seems that Wall Street is about to get a blockchain makeover. The U.S. has embarked on a journey to cement its dominance in digital assets—one that could fundamentally reshape how financial markets operate. At stake is nothing less than America's position as the world's financial capital, and the early signs suggest this is no minor regulatory adjustment but rather complete embrace of crypto's revolutionary potential.

The strategy is unfolding on two fronts. The Securities and Exchange Commission (SEC), under new leadership, is rewriting the regulatory playbook with new enthusiasm and support for crypto innovation. Congress, meanwhile, is crafting legislation to end years of jurisdictional squabbling. Both efforts will serve President Trump's declared goal: making America the "crypto capital of the world" and luring back the businesses that fled during the previous regulatory winter.

From prosecutor to promoter

The SEC's regulatory pivot begins with "Project Crypto," the brainchild of its new Chair Paul Atkins. Analysts at Bernstein have described it as the "boldest crypto vision ever laid out by a sitting SEC chair"—high praise indeed, given the agency's historically frosty relationship with digital assets.

Hopefully, the days of "regulation by enforcement," that crude approach of letting lawsuits clarify the rules, are gone, once and for all. In its place comes a comprehensive framework designed for the digital age. The project will enable 24-hour markets, instant settlement, and put an end to the regulatory limbo that drove crypto firms offshore.

The “Project Crypto” initiative's five pillars reveal its regulatory ambitions. First, it will bring crypto fundraising back to American shores, discouraging the elaborate offshore structures that one observer dismissed as "decentralisation kabuki theatre." Second, self-custody rights will gain explicit protection, challenging previous guidance that treated personal crypto wallets with suspicion.

Most intriguing to us, Project Crypto envisions "super apps"—financial platforms offering everything from traditional securities to crypto lending under a single federal licence. The promise of regulatory one-stop shopping could prove irresistible to firms tired of dealing with America's state-by-state requirements.

The proposal also acknowledges reality: not all blockchain systems are fully decentralised, nor need they be. This sensible and realistic stance could end the industry's pretence of complete decentralisation—a charade maintained solely for regulatory compliance. Finally, an "innovation sandbox" would allow new business models to launch quickly, even if they don't neatly fit the “existing rules and regulations.”

Congress weighs in

The legislative effort centres on the Digital Asset Market Clarity Act (CLARITY Act), which passed the House with something we don’t see much of anymore - bipartisan support. The 236-page bill attempts to solve crypto's most vexing problem: which regulator oversees what.

The proposal is surprisingly simple in concept, though complex in execution. A blockchain-based digital asset is considered a security by default and regulated by the SEC until it is determined to be part of a mature blockchain system—and therefore a digital commodity regulated by the Commodity Futures Trading Commission (CFTC). To qualify as a digital commodity, the bill requires the asset issuer to file a notice with the SEC and demonstrate that the digital asset meets specific decentralization requirements. A key requirement is that no single person or group can control the blockchain system through 20% or more of the voting power or token ownership. If a new blockchain project is centralized but aims to become decentralized (achieving "mature blockchain system" status) within four years, its digital assets will remain primarily under SEC regulation until it reaches that mature status.

The bill also tackles a persistent headache for developers. The proposed Blockchain Regulatory Certainty Act, included in the CLARITY Act, would exempt non-custodial software creators from money transmission requirements—a change that could unleash a wave of innovation in decentralized finance.

The winners’ circle

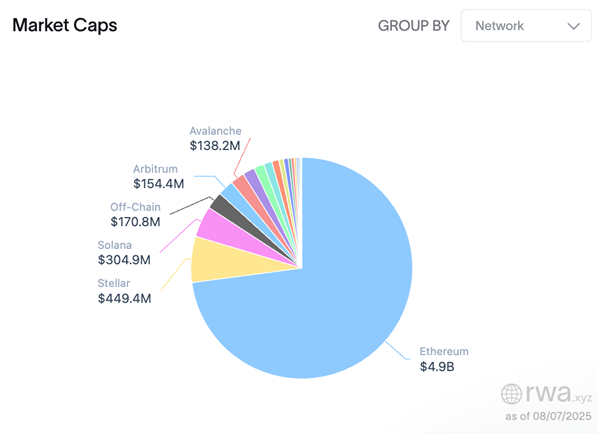

If the bill passes the Senate and is implemented, these reforms will create clear winners. Ethereum's ecosystem appears particularly well-positioned. The SEC's push to move financial markets "on-chain" plays directly to Ethereum's strengths: its established infrastructure, dominance in stablecoin issuance, and foundation for major Layer 2 solutions, such as Arbitrum and Base. A decade of uninterrupted network uptime has earned Wall Street's respect and trust. Currently about 54% of stablecoins and 73% of tokenized US Treasuries are issued on Ethereum.

Tokenized US Treasuries, bonds, and cash-equivalents by network

Source: RWA.xyz

Decentralized finance (DeFi) protocols also stand to gain legal clarity. The explicit acknowledgement of both truly decentralised systems and those with controlling operators signals an end to regulatory charades. The CLARITY Act's exemptions for non-custodial platforms, like crypto exchange Uniswap, would further cement DeFi's legitimacy.

A separate SEC statement declaring that liquid staking activities are not securities is a big deal for the DeFi sector. Such regulatory clarity is likely to unleash innovation in liquid staking tokens—financial instruments that allow investors to earn rewards while keeping assets liquid. Developers could freely experiment across lending, trading, and restaking protocols, while crypto ETFs and corporate treasuries would likely stake their tokens. The result: enhanced capital efficiency and composability in DeFi.

Meanwhile, tokenization of traditional assets by Wall Street will continue to accelerate. Project Crypto explicitly supports tokenized capital markets across stocks, bonds, partnership interests, and other financial securities while the CLARITY Act would make it easier for banks to offer digital asset custody—overriding years of the SEC’s restrictive guidance.

The sceptics speak

There are two sides to every coin, pun intended. Timothy Massad, a former CFTC chairman, warns that the CLARITY Act's complexity could create more problems than it solves. Its intricate definitions might enable "regulatory arbitrage," he argues, as firms shop for the lightest regulatory touch.

The concerns extend beyond mere complexity. Shifting oversight to the CFTC—a smaller agency with a different mandate—might weaken investor protection, particularly for retail participants. The CFTC would be tasked to oversee cash or spot market transactions in digital commodities, a marked departure from its traditional focus primarily on derivatives markets . The pseudonymous nature of blockchain addresses makes it difficult for the agency to monitor whether a person or entity has quietly acquired more than 20% of token ownership. Consequently, the CFTC would require substantial additional resources to effectively regulate digital commodities.

The bill's exemptions for decentralized finance could create regulatory gaps, allowing traditional financial activities to migrate to supposedly unregulated platforms. The bill has also been criticized for failing to prohibit proprietary trading by digital commodity exchanges, which can lead to conflicts of interest such as front-running customer orders—a practice generally prohibited in regulated securities and derivatives markets.

Even Project Crypto faces questions about its durability. The proposals remain largely aspirational, lacking the formal rulemaking process that would cement them into law. A future administration could easily reverse course, leaving the industry in familiar uncertainty.

Adding to the complications, President Trump's own crypto ventures—including meme coins—have drawn criticism for conflating public service with private profit. Such entanglements risk casting a shadow over otherwise legitimate policy efforts and fintech innovations.

The path ahead

It’s about time the US finally comes to terms with the inevitable, that is, a future with digital assets and blockchain as both the centre and foundation of the global financial system. The country that invented modern capital markets now seeks to reinvent them for the digital age. Early market reactions suggest investors are on board—crypto prices have soared since the presidential election, and traditional financial institutions are eagerly announcing and launching new crypto products.

Yet ambition alone guarantees nothing. The initiatives' success will depend on careful implementation, seamless inter-agency coordination, and lawmakers' ability to foster innovation while protecting investors. The regulatory revolution may be beginning, but its outcome will be an evolving state.

The stakes are high. Success would cement American leadership in a technology that promises to reshape finance globally. Failure would hand that advantage to competing jurisdictions already moving aggressively into the space—Switzerland with its crypto-friendly regulations, Singapore's institutional-grade digital asset hub, and the UAE's ambitious blockchain initiatives in Dubai. In the race to define digital finance's future, America has chosen to compete rather than cede ground to these well-positioned rivals. Whether it can do so without compromising the integrity that made its capital market the world's largest and most trusted remains the ultimate test.