Summer of Institutional Adoption

June 2025 Commentary

As we approach the summer months, a lackluster crypto market in June may suggest that cryptoasset denizens are away on travel or at the beach. Nothing could be further away from the truth. Stablecoin legislation progressing through the US Senate, corporate treasuries adding bitcoin and other tokens, and real-world assets (RWAs) accumulating on-chain are all indicators that adoption has been anything but lethargic.

The digital assets market cap grew just about 1% over June but that belied the underlying volatility. Investors were quick to take risk off the table in response to Israel’s attack on Iran’s military bases and nuclear facilities in mid-June, and following the subsequent bombing of Iran’s nuclear plants by the US. However, the markets quickly stabilized after US President Trump announced a ceasefire a few short days later.

While the markets wobbled, lawmakers, corporations, and financiers were busy at work.

CRCL, a GENIUS Act in the Right Place, at the Right Time

Stablecoins, cryptocurrencies pegged to fiat currencies, mostly the USD, have been touted by many as the cryptoassets with the best product-to-market fit. Over the last 5 years since the DeFi summer of 2020, the most durable type has been those backed by TradFi cash or cash equivalents. For the DeFi economy, stablecoins offer traders and investors the ability to hold their assets in “cash” with close to zero volatility, and to transfer value across wallets or platforms at close to no fees. Over the past year, combined stablecoin market cap has grown from about $155 billion to nearly $264 billion, or about a 70% increase, according to CoinGecko. Yet for all its size, regulation over stablecoins have remained in a gray area in the US.

That’s all about to change. On June 17, the US Senate passed [1, 2] the GENIUS Act with an overwhelming majority of 68-30. The Act sets up a regulatory framework for the issuance of payment stablecoins. Only “permitted issuers may issue a payment stablecoin in the United States. Permitted issuers must be a subsidiary of an insured depository institution, a federal-qualified nonbank payment stablecoin issuer, or a state-qualified payment stablecoin issuer. … Permitted issuers must maintain reserves backing the stablecoin on a one-to-one basis using U.S. currency or other similarly liquid assets, as specified.” [3] The bill still needs to be reconciled with the Congressional House’s version and a final version needs to be voted upon before it is passed to the President for final approval. Nonetheless, this was a significant step forward.

It's no wonder that Circle Internet Group chose this auspicious moment to IPO their equity (CRCL). Circle is well known for its stablecoin, USDC, which is the second largest stablecoin with a market capitalization of $62 billion in circulation over the Ethereum and other blockchains, and its other lesser known stablecoin EURC. Although Circle priced its IPO at $31/share, the first day of trading on June 5 saw investors quickly push its price to close at $83. CRCL’s share price would go on to reach a high of over $263. At the time of this writing, CRCL was priced at around $189, with a market cap of $41 billion. This makes CRCL eye-wateringly expensive with a forward price/earnings (P/E) ratio of 156x even when compared to a tech darling like Nvidia (NVDA) which trades with a forward P/E of a mere 37x.

CT^2: Corporate Treasuries Juicing on Crypto Tokens

Corporate treasuries typically hold assets that are sensible for their business operations. A quick glance at Ford Motor Company’s balance sheet in its March 2025 10-Q shows that among its assets, it holds cash and equivalents, marketable securities (invested for yield generation), and trade and finance receivables. For a digital assets company such as MARA Holdings, a Bitcoin miner formerly known as Marathon Digital, its March 2025 10-Q shows that it holds cash and equivalents, and digital assets, namely BTC. This makes sense as the company receives BTC for its work and has chosen to retain excess BTC it does not need to convert into fiat USD. Tesla broke the mold by previously accepting BTC as payment for its vehicles, and while it no longer does so, it still holds BTC on its balance sheet.

Tesla may be the groundbreaker with regards to being a non-digital assets native company to hold digital assets in its treasury, but Strategy (MSTR) blew the doors open by converting its enterprise analytics company into an outright vehicle for holding BTC. According to its March 2025 10-Q, BTC holdings total $43.55 of the $43.92 billion of Total Assets. Quarterly revenues from software licensing and subscriptions of $111 million were swamped by an unrealized loss of $5.9 billion on digital assets. At this point, equity investors of MSTR no longer cared about its earnings and were happy to pay a premium of close to 4x book over its holding of BTC.

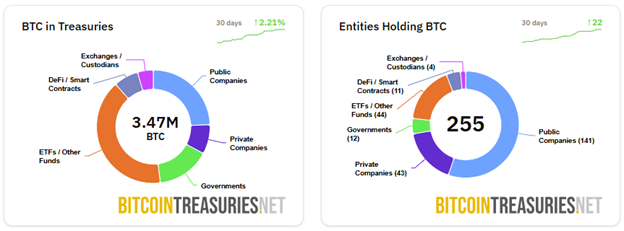

Other corporate executives were quick to take note of the equity share premium that investors were willing to pay for crypto tokens held in corporate treasuries. Over 2024, companies like Semler Scientific, a medical technology company, and Metaplanet, a Japanese hotel operator, followed suit by adding BTC to their respective treasuries. According to BitcoinTreasuries.net, publicly listed companies comprise over half of the entities holding about a quarter of the BTC across various entities being tracked including governments and ETFs.

Source: bitcointreasuries.net

What’s been more notable recently is that on May 27 of this year, Sharplink Gaming (SBET), a sports betting technology platform that lost money over the last three years, announced that it will raise capital to hold ETH in its treasury. Its stock price rocketed close to $80 upon announcement, and while it has retraced back to just above $12, this is still significantly higher than its recent lows of below $3.

SBET, source: Nasdaq.com

The expanding trend to hold other cryptoassets is just beginning, with other companies looking to hold SOL and XRP in their treasuries. How this will play out is far from clear. On one hand, one can look upon this as share gimmickry to boost share prices to multiples above their book values. More nefariously, as companies issue equity, convertibles, and debt to purchase digital assets, it evokes 2022 as leveraged loans, collateralized by crypto assets, were issued to buy more cryptoassets. However, this time is slightly different for a couple of reasons. First, these are publicly listed companies which are required to be transparent about their corporate activities with their annual and quarterly filings, and updates on significant events. This is quite unlike the privately held crypto lending firms, the likes of Celsius and BlockFi, back in 2022. Second, as this article in the Global Treasurer pointed out, it will be the security holders who are first to face impairment and default risks, possibly drawing a line to prevent a contagion.

RWAs Showing Real Growth

Stablecoins backed by fiat currencies and cash equivalents, such as US TBills, are the most basic form of real-world assets (RWAs) brought onto the blockchain. Aside from stablecoins, blockchain firms have continued to add longer-dated US Treasuries and private credit on-chain. Over the past year, the amount of RWAs has roughly doubled to over $24 billion.

Source: rwa.xyz

What’s hard to see in the chart above but is quite significant is the amount of tokenized stocks at the bottom in the bright pink line. Currently, tokenized stocks make up only $426 million. While this is a pittance compared to the total of $24 billion of RWAs, it is noteworthy that this is a space that Robinhood, a fintech brokerage platform, has entered. On June 30, Robinhood announced, it had “launched US stock and ETF tokens in the EU, giving eligible customers exposure to US equities with Robinhood Stock Tokens—featuring zero commissions or added spreads from Robinhood (other fees may apply), dividend support, and 24/5 access. With tokenized stocks, our European app transitions from being a crypto-only app to an all-in-one investment app powered by crypto. European customers will have access to 200+ US stock and ETF tokens. Stock token holders will also receive dividend payments directly in their app.”

This announcement ought to be the wake-up call for all TradFi firms – brokerages, custodians, and depositary institutions alike. Simply said, traditional assets are now moving onto blockchain rails. Many are paying attention. The publication Chief Investment Officer released an article on tokenization on July 1. It cited the many benefits of asset tokenization including improving liquidity, expanding investor access to a broader set of assets, and near-instant settlement – all benefits that we have previously espoused and discussed.

Investors may currently be distracted by macro events. The US had made a lot of noise with its new budget signed back on July 4. The ceasefire in the Middle East remains uneasy and Ukraine is still under attack. Come August 1, we may be hearing what kind of reciprocal tariffs the US will be imposing on its trading partners. But for digital asset investors, the important developments are in the quickly blurring lines separating TradFi vs Blockchain and DeFi.