Consider Fat Tails for Setting Guardrails

January Commentary

After a soft January, the crypto markets sold off sharply in the first week of February. BTC dropped to a low of $62,822 on February 5 (a 50% drop from its October 2025 high of $126,080) before recovering to around $70,000. Many commentators have noted that this is one of the rare multi-standard deviation events, but empirical evidence suggests that oversized negative and positive returns occur more often than what a simple standard deviation metric would suggest. This has implications for portfolio positioning and holding horizons.

Abnormal Fat Tails

Calculating the first two moments (average and standard deviation) of a time series of price returns is a quick way to characterize and understand price behavior. The emphasis, however, is on the “quick”. Stopping there and not looking at the skewness and kurtosis (fatness of the distribution tails) assumes that the returns fall into a normal (aka, Gaussian) distribution and can lead one to miss the bigger picture.

BTC and other token price returns are perfect examples of this.

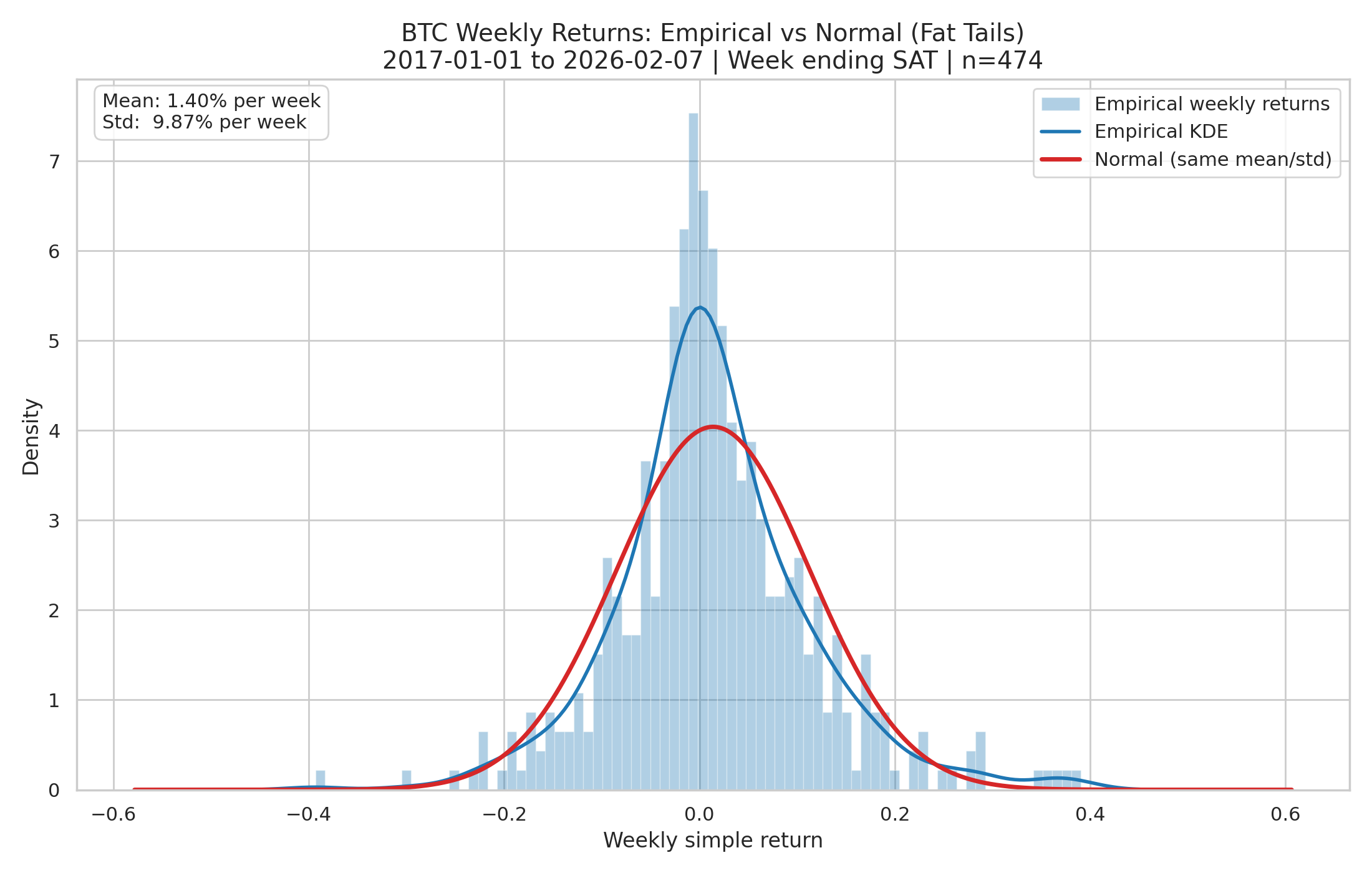

Empirical vs. normal distribution of weekly returns. Sources: CoinGecko, Firinne Capital

Looking at the weekly returns of BTC over the last 9-plus years, we measure that weekly returns have averaged +1.40% with a weekly standard deviation of 9.87%. The returns also exhibit a skewness of +0.39, owing partly to the fact that 54% of the returns are positive. It also has an excess kurtosis of +2.13, indicating more positive and negative tail returns observed than expected with a normal distribution.

BTC’s selloff of 17.65% in the first week of February was close to a 2-sigma (i.e., standard deviation) loss. Empirically, we should expect such a loss over a week about once every 7 ½ months. What is worth paying attention to are losses of 28% or more in a week, a 3-sigma event. A normal distribution suggests that this would occur once every 14 years. Empirically, it is likely to happen closer to once every 2 ½ years.

“The market can stay irrational longer than you can stay solvent.”

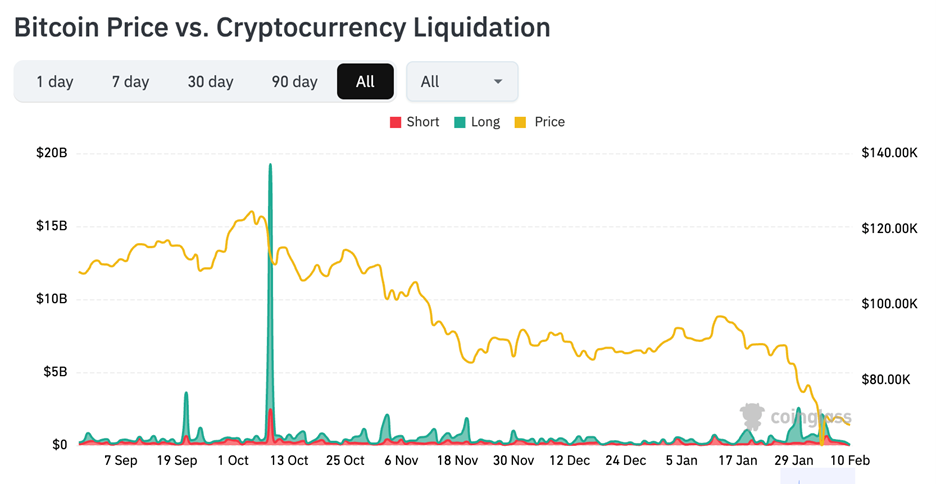

Fast price declines within a short time window are typically characteristics of leverage long positions being liquidated. The decline over the last three weeks is no exception, although the overall magnitude pales in comparison with the October 10, 2025 liquidations of $19 billion.

Liquidation history with green bars indicating liquidation of long leveraged positions and red of short leveraged positions. Source: CoinGlass

Many analysts have also pointed out the close correlation between the recent drop in BTC prices with the drop in software company prices. The exact causes are not transparent but has been hypothesized to come from Fed policy risk, AI and quantum risk, and declines in risk appetite among institutional investors.

Back to Fundamentals

Fundamentally, we remain optimistic about crypto markets in 2026, but this view is one of a longer horizon while the markets tend to react to the shorter-term news cycles.

We are bullish about the market because the underlying blockchain technology and the applications that the tokens represent are still early technology protocols and platforms that will take time to adopt and implement. This process has not been steady, and you can characterize the attitudes prior to 2024 as denial, trivialization, and sometimes criminalization. The results of the 2024 election have, on balance, ushered in a more positive tone for the crypto industry on the regulatory, legislative, and institutional adoption fronts.

As evidence of the legislative progress, the GENIUS Act was passed quickly in July 2025, just 6 months into the new Republican led administration, to regulate stablecoin issuance in the US. While significant, this currently covers “only” $300 billion in stablecoin market capitalization compared to the broader $2.3 trillion value of tokens that are trading. The CLARITY Act, however, is a bill that is intended to cover the crypto market infrastructure and tackles a wide range of issues from privacy, KYC (Know Your Client), AML (anti-money laundering), the role of DeFi, and yield-bearing stablecoins. Due to its encompassing nature, this is a more complex bill to negotiate and is currently stalled [1, 2] in the US Senate as legislators and the President continue to work with the banking and the crypto industries over their differences.

Similarly on the regulatory front, the new Chairman of the SEC, Paul Atkins, has been demonstrably more supportive of the crypto industry. Crypto Innovation was core to one of his earlier speeches back in May 2025. He followed up in July with a discussion of providing an “innovation exemption”, a sandbox if you will, for businesses to go to market with new products and services, and was expecting to roll this out in January 2026. Unfortunately, timelines tend to be optimistic while the realities of working out the details and finding compromise across different stakeholders tend to take time. As of a week ago, the delivery time for this innovation exemption is still unknown.

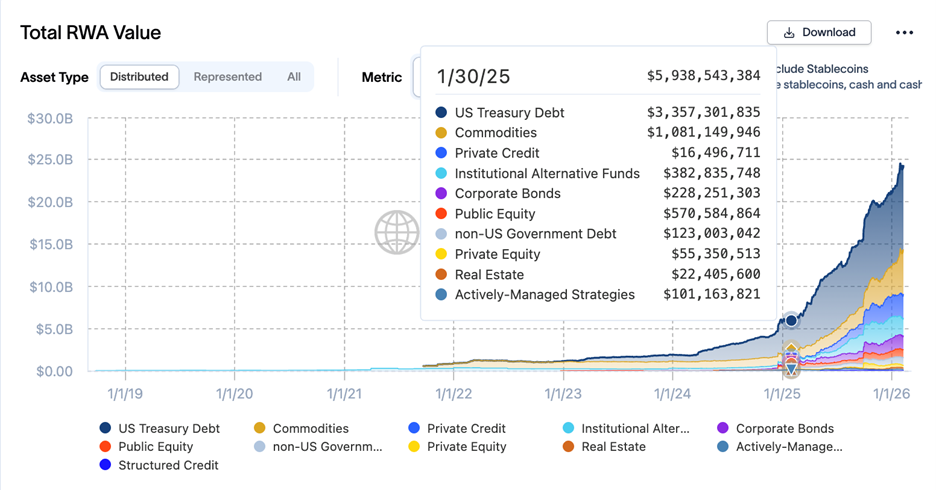

Finally, the institutional interest in adopting blockchain technology as their settlement layer has been active, as has been for issuing tokenized securities. DTCC is the settlement layer for global trading of equity and bond securities, and in December 2025, they received a no-action letter from the SEC (effectively a statement from the SEC stating that they will not take up enforcement actions against certain activities) for their efforts to tokenize US securities. The interest from institutions in pursuing tokenization is evident in the growth of the assets that have been tokenized. Over the past 12 months, this has grown about 4-fold from $6 billion to currently just under $24 billion.

Source: rwa.xyz

These are the fundamental reasons as to why we are bullish. However, the shorter-term news cycles, from tariff announcements and immigration to how the US is dealing with its allies, are leading to uncertainty. Uncertainty is disruptive to the pricing of risk assets and leads to higher volatility in the market. Short-term investors hoping for quick profits, especially ones who use leverage, and digital asset treasury (DAT) companies recently formed in the past year don’t necessarily have this long-horizon mindset. They become the marginal traders, boosting prices during price increases but demanding liquidity on price pullbacks. We feel that currently the upside potential outweighs the downside risk, but it will be the long-term investor who can stand to benefit by appropriately positioning their portfolio to withstand the near-term volatility.

Portfolio Implications

What’s a long-term optimistic investor to do in this environment? If the investor were to size a portfolio assuming a normal curve for returns, they will systematically under-budget for the frequency of extreme weeks and under-estimate the risk to their portfolio.

Solvency is paramount to surviving outsized returns. Avoiding excess leverage (or leverage at all) avoids exposure to forced de-risking by liquidation. Since fat tails exist on both the left and right sides of the distribution, being able to “stay in the game” means being able to share in the gains when liquidity returns to the market.